News: Northern New England

Posted: September 4, 2020

Are the markets up, down, or sideways? - by Thomas House

Are the markets up, down, or sideways?

You could be forgiven for rolling your eyes and saying “Sideways. Duh.”

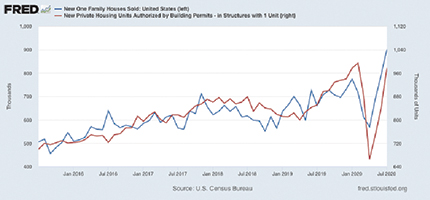

But before you do, note that the July single housing sales has reached the levels of around 2000, and the highest since 2006.

And same for the initial pandemic panic, single family sales and permits have both returned to the status quo ante.

Juiced, a bit, by record low mortgage rates.

So the sky is not falling. But neither is that sky blue.

The cloud on the horizon: multifamily paints a different story

U.S. Census Bureau / fred.stlouisfed.org

The gathering storm is in multifamily, vacancies rose slightly to 4.6% while rent fell by 1.4% - with ongoing covid-related rent moratoria and (very) high unemployment adding to the uncertainty.

Mixed use developments face the added pressure of retail closures and office distancing, it takes no imagination at all to see this going sideways for the moment. Commercial spaces need to adapt to accommodate distancing and other health factors going forward.

Like all storms, it will be of limited duration - maybe only a squall line - of related depressed activity and economic circulation.

Recovery is more related to epidemiological considerations than to pure market forces. Our view is this will eventually create pent-up demand - and a need for architects to change design to meet the need.

Timing is everything, and now’s time

There are design factors developers need to take into account - but now there is the time for developers and designers to improve multifamily and mixed use valuation by reducing common area exposure; for one example, entrances and hallways may need to move out of doors, including the possibility of ground level entrances on individual units.

The post-pandemic value proposition is that transmission of common (but societally costly) contagions such as the flu and the common cold will almost certainly be reduced.

All this comes with cost considerations, especially when contemplating controlled access, to say nothing of mechanical requirements in order to provide ventilation, entertainment space, hands-free and app-based controls, and even laundry in individual units.

Lost will be the efficiencies gained by common hallways, amenities, and building utilities - but those are likely now to become liabilities in need of (cha-ching!) remediation.

WorkForce Housing / courtesy THA Architects LLC

The new normal? Not yet.

For multifamily housing there will be pent-up demand, especially in Boston where stats are down, but the city and its inner suburbs are slightly underbuilt. Plus Boston is fifth-ranked nationally by CBRE for Q2 with a positive absorption rate.

This cloud will lift once the freshening breezes of economic conditions come onshore, and various protections are no longer needed.

Mixed use, however, poses some longer term problems. Where the public or employees meet, a longer memory will persist. Lockdown work-from-home conditions won’t last long at scale, it will almost certainly be a rolling or partial consideration going forward. No employer wants the liability, and no employee wants this disease or any other.

To be clear, the unemployment rate remains at nosebleed levels, worse than 2010, just less apocalyptic than a few months ago. Housing may have reached something resembling the status quo ante. The structural economy has a long way to go yet.

It is important for architects and developers to unbox their Pentels, roll out the trace, and begin innovating solutions to provide both palliative and real solutions to the endemic realities of contagious pathogens.

Because it won’t end with COVID-19, and we’ll all be better off if next time we’re prepared.

We can be part of the solution. A big part.

Thomas House, AIA, is principal of THA Architects, LLC, Stratham, N.H.

Tags:

Northern New England

MORE FROM Northern New England

PROCON and Hitchiner break ground on 57,000 s/f shared services operations facility

Milford, NH Hitchiner, in partnership with PROCON’s integrated design and construction team, has officially broken ground on a new 57,000 s/f shared services operations facility at its Elm St. campus. This building will house value-added services used across Hitchiner’s various business units,