News: Financial Digest

Posted: June 17, 2016

Tolerances with the TILA-RESPA integrated disclosures from Consumer Financial Protection Bureau

Boston, MA Similar to existing law, the Consumer Financial Protection Bureau’s final TILA-RESPA rule restricts the circumstances in which consumers can be required to pay more for settlement services than the amount stated on their loan estimate.

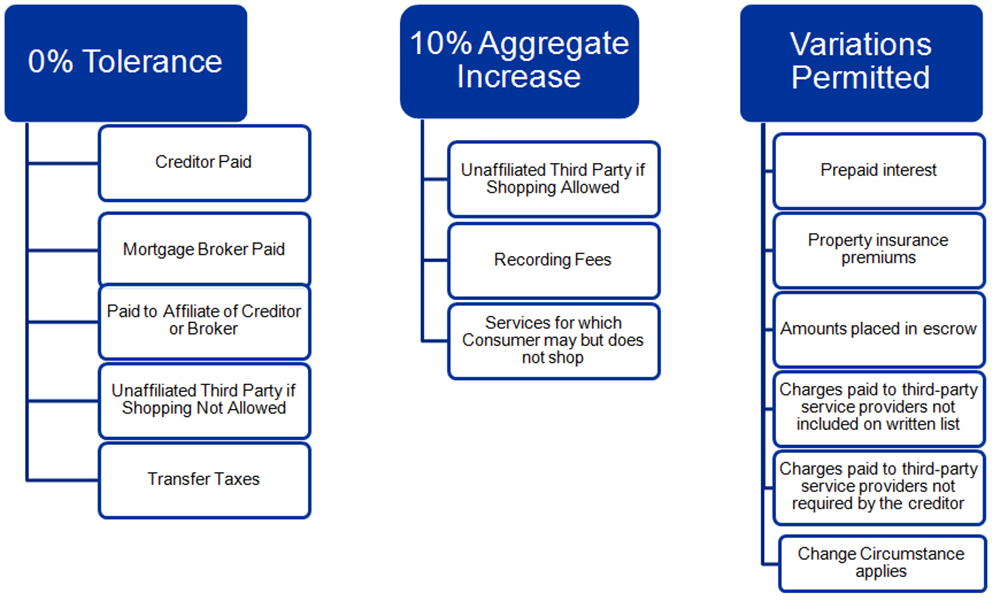

Generally, good faith requires the closing cost estimate on the initial loan estimate to equal the final amount charged on the closing disclosure. Here’s a look at which fees can and can’t change (see chart 1).

Chart 1

Chart 1In today’s current practices, many providers add a cushion for costs on the HUD-1 to account for items that can vary between the signing and when the transaction is settled after recording, such as recording fees, pro-rations and prepaid interest. The overage is then refunded after the final disbursements are made. Under the new rule, lenders and settlement agents must make more rigorous good-faith efforts to provide estimates that are more accurate. However, the delay between consummation and settlement in escrow states its likely to increase the need for post-closing corrected disclosures.

If the closing disclosure becomes inaccurate before consummation, the creditor shall send corrected disclosures so that the consumer received the corrected version at or before consummation. The changes are still subject to good faith requirements. Once the initial closing disclosure is issued, all changes should be made with an updated closing disclosure. The creditor may not provide a revised loan estimate on or after the date the creditor provides the consumer with the closing disclosure.

Under the new rule, if a lender allows a consumer to shop for a settlement service, the lender will be required to provide the consumer with a written list identifying available providers of that service and clearly stating that the consumer may choose a different provider for that service. The CFPB has provided a blank model form for the written list of settlement service providers, a sample of written list of providers consumers can shop for and a sample of written list of providers consumers cannot shop for.

What About Title Insurance?

According to the CFPB, owner’s title insurance that is not required by the creditor is not subject to the 10% variance. The CFPB said it is aware that the preamble to the final rule contains potentially conflicting language, but advises that the final rule text is what should be followed.

The 10% variance category includes recording fees and charges paid to unaffiliated third-party service providers when the consumer is permitted to shop for a settlement service provider, but chooses a provider from the creditor’s written list of providers (§ 1026.19(e)(3)(ii)).

Owner’s title insurance is not a charge that is assigned to a particular variance category. Therefore, the applicable variance category depends on other factors, including whether the creditor requires the insurance and, if so, whether the consumer may shop for the provider of the insurance.

To the extent owner’s title insurance is not required by the creditor and is disclosed as an optional service, under the rule the insurance is not subject to any percentage variation limitation, even if paid to an affiliate of the creditor.

Tags:

Financial Digest

MORE FROM Financial Digest

Preservation of Affordable Housing secures $23.5 million in financing from Rockland Trust and Citizens Bank

Cambridge, MA The nonprofit Preservation of Affordable Housing (POAH) has secured $23.5 million in financing from Rockland Trust and Citizens Bank to transform a 150-year-old, underutilized church complex into housing. The project will ultimately create 46 affordable family-sized apartments.

Columns and Thought Leadership

Examples of investors who used Kay Properties for legacy and estate planning purposes for rental property/portfolios - by Dwight Kay

Preserving wealth across multiple generations requires strategic planning, foresight, and the right investment vehicles. Delaware Statutory Trusts (DSTs) offer a powerful solution for families looking to build and protect their financial legacy and to efficiently plan for their estate.

Conn. hospitality market: A technical appraisal perspective on market dynamics and valuation challenges (2019-2025)

The Connecticut hospitality market has demonstrated uneven recovery patterns between 2019 and 2025, with boutique and historic properties achieving $125 RevPAR in 2025, up 8.7% from the 2019 level. Coastal resort properties achieved a $105 RevPAR in 2025, representing 10.5% growth since 2019. Casino corridor properties maintained modest growth with RevPAR improving 4.5% to $92 in 2025.